Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

from Malena CaroloCalMatters

This story was originally published by CalMatters. Sign up for their newsletters.

As California’s electricity rates remain nearly the highest in the nation, the state’s utility regulator is poised to reduce the payout shareholders can get from California’s big three investor-owned power companies.

In a decision proposalThe California Public Utilities Commission recommended a 0.35 percent reduction in “return on equity” each for Pacific Gas & Electric, Southern California Edison and San Diego Gas & Electric. If approved, shareholders of all three companies would see a potential return next year of just under 10%. Similar returns for PG&E and Edison have not fallen below double digits in at least 20 years.

Utilities said the downturn would affect their ability to make the necessary investments for their operations. Critics of the decision said the drop was too small to have a significant impact on payers’ bills, even if it was a step in the right direction.

“California and other (public utility commissions) allow rates of return that far exceed legal requirements,” said Mark Ellis, former chief economist at Sempra, which owns San Diego Gas & Electric.

The California Public Utilities Commission is expected to vote on the decision in December.

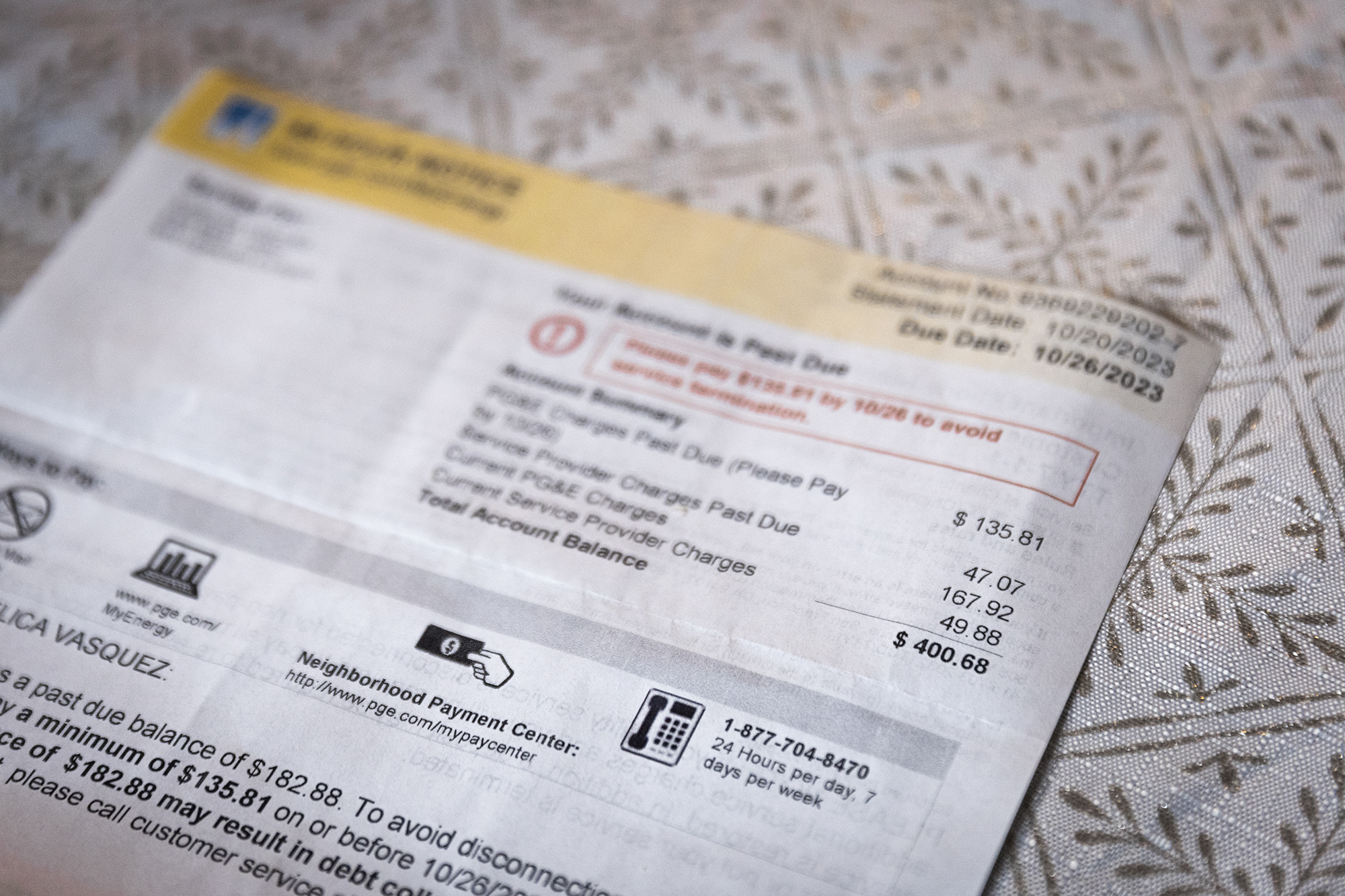

Californians pay the second highest electricity rates in the US after Hawaii, according to the latest data from the US Energy Information Administration. A number of factors go into these rates, including wildfire mitigation costs. PG&E in particular has drawn the ire of customers in California frequent interest rate hikes in the last year.

Embedded in these accounts is the return on capital, money intended to compensate shareholders about the risk of doing business. These shareholder return rates are set by each state’s utility regulators and hover nationally around 10%. If approved, PG&E’s rate would be 9.93% (down from 10.28%), Edison would be 9.98% (down from 10.33%), and San Diego Gas & Electric would be 9.88% (down from 10.23%). These rates are not automatically guaranteed – utilities may not achieve this return if they do not keep costs low, such as project overruns or unexpected litigation fees.

A small change in that rate could mean a difference of millions of dollars to payers. The return is a percentage of the rate base, the total value of the utility’s assets from which it can earn a return; this includes projects such as the construction of a new power plant for example. Rate fundamentals for California’s big three investor-owned utilities have steadily risen each year as they add new customers and projects, increasing the amount shareholders can receive.

PG&E, for example, had a 10% return to shareholders in 2023, a possible return of about $125 million. If it had been 1% lower, the potential return would have been $12.5 million less.

“The proposed cost of capital solution needs refinement to better reflect California’s unique risks and market realities,” Edison spokesman Jeff Montford said. “Incorporating these clarifications into the final decision will improve SCE’s ability to fund essential infrastructure projects for a more reliable, sustainable and ready electric grid.”

PG&E spokeswoman Jennifer Robison echoed that sentiment, saying the decision “does not recognize the current heightened risks to help attract needed investment for California’s power systems.”

Anthony Wagner, a spokesman for San Diego Gas & Electric, said, “A decision that accurately reflects these realities is essential to enable investments that reduce wildfire risk, increase reliability, replace aging infrastructure and advance California’s clean energy transition for the benefit of the communities we serve.”

Utilities routinely demand that these interest rates be raised because they are a key part of what goes into a utility’s credit rating, affecting the interest they pay on loans for infrastructure investments. But in recent years, experts and consumer advocates have pointed to a discrepancy — the utility industry is generally considered low-risk, but critics say the levels of shareholder returns don’t reflect that. Yields on 10-year U.S. Treasuries, considered the benchmark for a risk-free investment, are about half the national average for approved rates of return to utility shareholders. And it’s costing utility payers across the country up to $7 billion annuallyaccording to academics.

Ellis, the former Sempra economist, said there is a way to reduce shareholder returns while keeping customer accounts under control and maintaining credit ratings that the commission has not yet examined — changing the balance of debt and equity each company has.

“You really have to understand credits,” he said. “That’s where they’ll catch you.”

The commission has the right to determine the debt-equity balance when determining shareholder returns, but it left that unchanged for all three utilities in its proposed 2026 decision. Keeping shareholder return levels high as a primary means of maintaining high credit ratings, Ellis said, unnecessarily burdens ratepayers.

This article was originally published on CalMatters and is republished under Creative Commons Attribution-NonCommercial-No Derivatives license.